YOU ARE WHAT YOU MEASURE.

The measures by which anything — a person, an organization, a company — is judged drives its behavior. Fund managers have long focused on driving asset growth because assets under management (AUM) have historically been the standard by which they have been judged. In a business whose revenues come from asset-based fees, AUM should be an effective proxy for what ultimately counts most: asset managers’ revenue-generating potential.

This relationship between asset and revenue growth has frayed as fund buyers—both retail and institutional — have embraced lower-fee index funds as their appetites for higher-expense active strategies appears to have weakened. With assets growing fastest in places where fees are low, new AUM generates less revenue growth than it would have in earlier eras. A new white paper from ISS Market Intelligence, Growing Revenues, Not Assets, New Name of the Game, shows this reality playing out on both sides of the Atlantic, but with index fund market share crossing the 50% mark in 2023, the impact has been starkest in the United States.

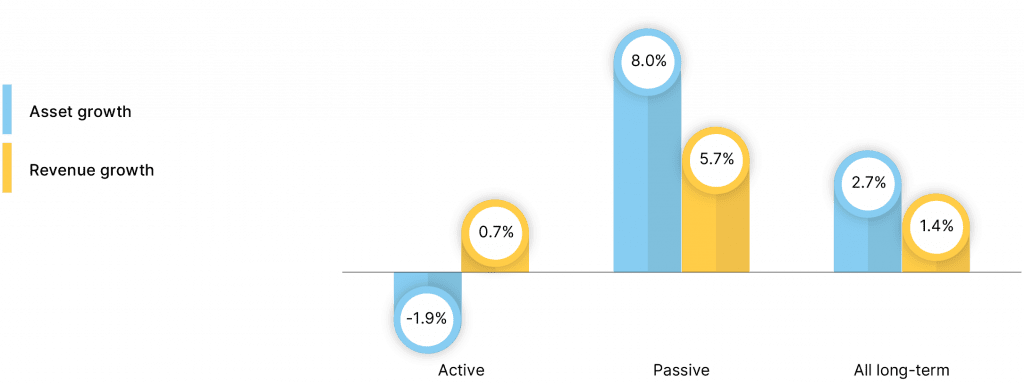

Of course, U.S. active fund managers have been coping with shrinking market share for decades, albeit with strong markets helping to soften the blow. Additionally, the erosion in market share has been relatively gradual, giving active managers room to adapt through product innovation, consolidation, and cost-cutting measures. Juiced by the proliferation of ETFs, the pace of the decline has accelerated in recent years, leaving active managers’ top lines under greater strain. Based on ISS MI’s estimates, long-term fund revenues generated by active funds fell 2% in 2023 as revenues from index funds rose 6% (see Figure 1).

Figure 1: Active Fund Revenues Under Pressure

Estimated growth in long-term fund revenues and average assets under management, 2023

Note: Data exclude money market and fund of funds.

FROM A TRICKLE TO A FLOOD

Almost 35 years after Vanguard founder John C. Bogle introduced the country’s first retail index fund in 1976, active managers still controlled more than 75% of long-term AUM.

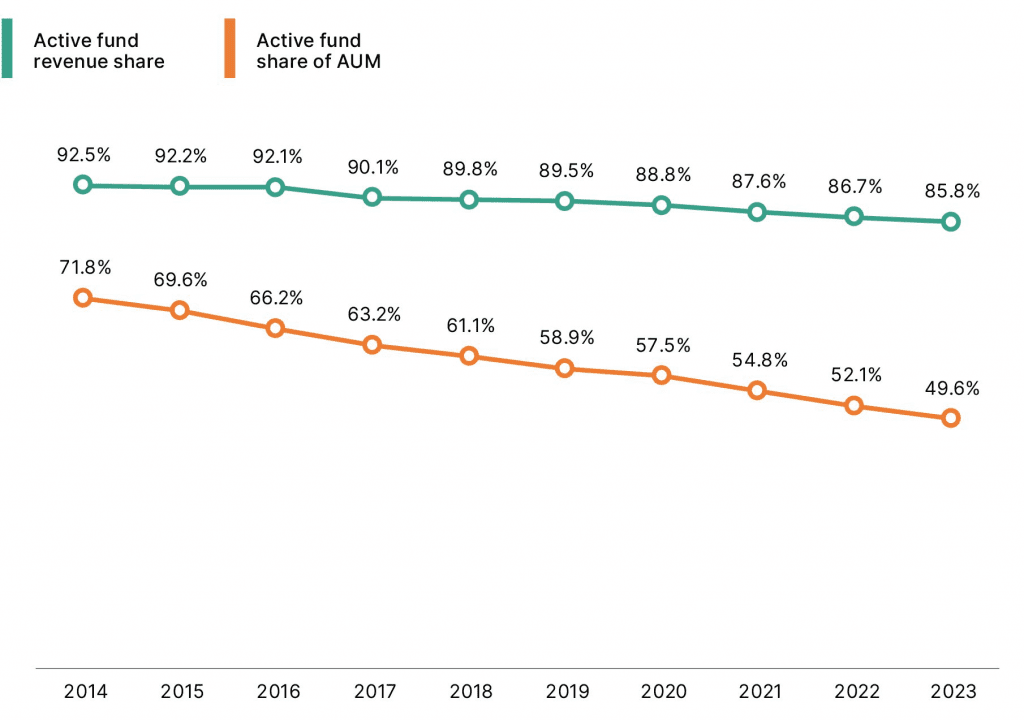

However, as the thirst for lower-fee investments reduced demand for active management in the 2010s, active funds shed nearly as much market share as they had in the prior 40 years. To be sure, the seemingly never-ending post-financial crisis bull market run, during which investors enjoyed 13 years of growth with modest and short-lived dips, gave the broad-based equity index offerings time to entrench themselves in the advisor and investor psyche. Regardless of the reasons, Figure 2 shows active fund share slipping to 50% by the end of 2023, down from 72% at the end of 2014. To paraphrase a character in Ernest Hemingway’s The Sun Also Rises description of his path to bankruptcy, active managers lost their dominance gradually, and then suddenly.

Figure 2: Despite Rapidly Declining Market Share, U.S. Active Funds Still Dominant Revenue Generators

Estimated share of U.S. long-term fund revenues, assets under management, 2014-2023

Note: Data exclude money market and fund of funds.

Index funds may have usurped active management’s market share supremacy in terms of AUM, but not revenues: Despite finishing 2023 with just under 50% of AUM, active funds delivered approximately 86% of revenues generated by long-term funds. For all the doubts surrounding the future of active management, it is the industry’s primary revenue engine — and likely will remain so for years to come.

While this still-vast revenue pool should support a healthy active fund market, persistent outflows will threaten managers struggling to grow organically. Such pressures have intensified in recent years as active managers’ revenue share has declined at an accelerating pace. The pie grew fast enough in 2021 to blunt the impact; thanks to the rebounding post-COVID market, active fund revenues rose approximately 16% even as market share slid nearly 1.5 percentage points. However, as the sharp rise in interest rates drove markets down in 2022, active managers suffered record outflows ($923 billion, 6% of beginning period AUM), abating only modestly in 2023 ($438 billion in outflows representing 3.5% of beginning AUM).

Meanwhile, pricing pressures intensified the strain. Active fund buyers continued to favor lower-cost strategies, which helped drive the average active fund expense ratio to an estimated 0.60% on an asset-weighted basis in 2023—a 36% decline from 0.80% in 2013. Weak AUM growth and falling fees is a recipe for sputtering revenue growth.

CHARTING EXPANSIONARY PATHS

If the past year teaches us anything, it is that the old game of maximizing the size of the asset base is a strategy that is well past its sell-by date. Not all asset growth is created equal, and it has become more unequal as the sales gap between active and passive funds has widened into a chasm in recent years.

Rather, managers need to focus on where the prospects for revenue growth are greatest and identify opportunities to improve scale where growth prospects are weakest. Certainly, there is no single recipe for victory. Some will find success through nascent—at least in the retail market—asset classes, such as alternatives. Others will do so by translating their capabilities to non-mutual fund vehicles, be it ETFs, fund models, separately managed accounts (SMAs), direct indexing programs or other private structures. Strong demand for active ETFs is a sign that investors have not given up on active management, at least when it is priced right.

Other managers will choose to operate across the value chain, as partners with advice providers or as distributors/wealth managers themselves. And some will leverage technology to shore up their own value chains and also support those of their distribution partners or even their direct competitors (for an example of this strategy, look no further than BlackRock’s Aladdin). A handful will thrive in all four. Either way, asset managers will need to identify their core strengths and identify innovative ways to distribute them in order to succeed.

The full global white paper Growing Revenues, Not Assets, New Name of the Game is available via MarketSage from ISS Market Intelligence.

By: Christopher Davis, Benjamin Reed-Hurwitz