While liquid alternatives have existed in some form for over two decades, the strong performance of equities during the bull market of the 2010s and the perceived underperformance of alts over the same period eroded investor interest in this asset class. The last several years, however, have seen renewed interest in alternatives, as the COVID-19 pandemic shocked markets; recent geopolitical crises have turned equity markets sideways; and rising interest rates have cratered the long-stable bond market. On top of recent macro-economic developments, education about and access to liquid alternatives has never been higher, with over 200 funds launched since the start of 2020.

Investor interest in liquid alternatives perked up in 2021, and despite (or perhaps because of) 2022’s down market, the asset class was a rare bright spot in an otherwise dismal year for fund sales. The funds attracted $47 billion in net sales in 2022, a touch less than 2021’s record haul. Organic growth, or the rate of flows relative to assets under management (AUM) at the start of the year, reached 15% last year. By contrast, overall long-term fund flows shrunk at a 1.8% rate.

We expect demand will remain strong in the years ahead. ISS MI’s 2023-2027 outlook, detailed in the recently published State of the Market: Future of Retail Products report, projects nearly $240 billion in alternative fund flows over five years, a 12% annual organic growth rate. On the back of brisk sales, AUM is projected to rise 15% annually to almost $620 billion (see the chart below).

Also anticipating rapid growth, asset managers have bulked up their product shelves with more options across investment areas and product types in recent years. In 2022, for example, managers brought a diverse mix of strategies to market. The 48 liquid alts funds managers launched last year spanned 18 different Morningstar categories, ranging from Nontraditional Bond to Digital Assets. The new launches have been concentrated in ETFs, and the asset class has been a prime contributor to the proliferation of active ETFs. Since 2020, fund managers debuted 160 new active ETFs, with active ETFs accounting for nearly two-thirds of liquid alt fund launches.

As fund buyer interest in private alternatives grows, concerns over access, fees, and liquidity remain

In addition to developments in the liquid alternative space, private market alternatives continue to attract heightened attention, driven both by investor demand and new avenues of access to alternatives. While private alternatives face significant regulatory headwinds limiting access to individual investors, they have nevertheless continued to draw considerable interest A mid-2022 survey conducted by ISS MI Market Metrics showed that the number of advisors who reported investing client dollars in private alternatives rising three percentage points (from 39% to 42%) in just six months, with non-traded REITs, private equity, private credit, and hedge funds all seeing increased investments.

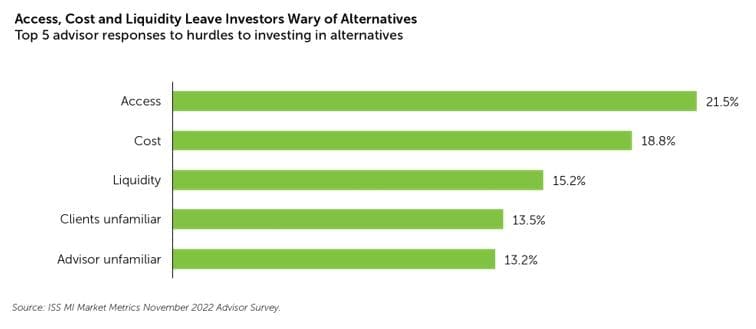

While the survey, which included responses from more than 300 participants, displayed advisors’ growing comfort with private alternatives, it also revealed barriers to further adoption. As one advisor put it, “High fees are not attractive to clients and raise the overall management fees. The illiquidity of many alternatives also is a deterrent. The audit requirements are also challenging.” These sentiments are not unusual among surveyed advisors. Along with access, advisors named cost and liquidity as the biggest hurdles to investing in alternatives, as the chart below illustrates.

While liquid alternatives address these challenges by offering daily liquidity, zero performance fees, and comparative ease of access for retail investors, they fail to capture the full depth of the alternative market. In part, that is because of regulations that prevent mutual funds from investing significant assets in the illiquid investments typically held by private equity, credit, real estate, and venture capital shops. In addition, private market fund managers have been slower to pursue the retail market, which is a more fragmented market that lacks the scale and sophistication of traditional institutional buyers.

The difficulty that retail investors face in accessing lower-correlation assets has coincided with a shrinking opportunity set for the retail market, as the number of publicly-traded firms has declined over the past two decades and as more IPOs happen later in companies’ life cycles. These have direct consequences on how extensively retail investors can diversify their portfolios.

Traditional asset managers, large private market players, and smaller upstarts have responded with solutions that address concerns of both fund buyers and sellers. Other ways to distribute alternative strategies, such as interval funds and online marketplaces providing lower-minimum access to private market funds, have grown considerably in recent years. These venues have broadened access to more mainstream areas of the private market (such as infrastructure and real estate) as well as harder-to-access niches (like modern art).

The emergence of solutions like these point to the new ways in which fund managers will need to compete. The future will require managers to develop a broad set of differentiated capabilities and distribute them in new ways. Whether through traditional mutual funds and ETFs, or interval funds and digital platforms, tomorrow’s successes will accrue to managers that can ply their crafts across many venues all at once.

_________________

Simfund Enterprise subscribers can access the State of the Market: Future of Retail Products on the Simfund Research portal. For more information about this report, or any of ISS MI’s research offerings, please contact us.

By: Liam Stewart, Senior Research Analyst, ISS Market Intelligence