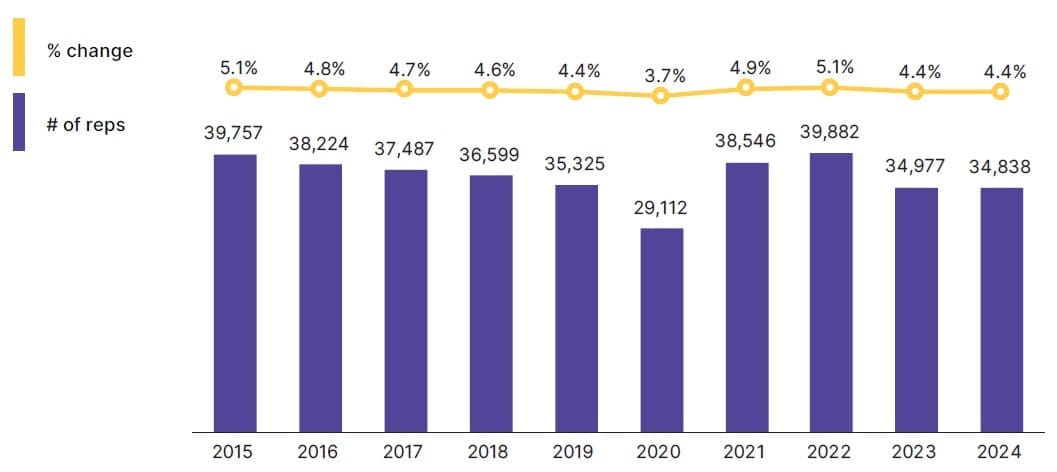

The financial advisory business, in the United States, is in constant flux. Indeed, thousands of registered reps switch firms each year in pursuit of better opportunities, business models, and client alignment. Data from ISS MI’s just-published Rep Movement Report shows that 2024 was no different: Nearly 35,000 U.S. based reps joined another firm in 2024—about as many as in 2023.

In any given year, around 4% to 5% of reps depart to other firms. Turnover clocked in at the higher end of this range in 2021 and 2022 following the COVID-19 pandemic after registering well below normal levels in 2020. The chart below, which depicts historical rep movement, shows turnover returning to more modest levels in 2023 and 2004.

Figure 1: Back to Normal: Rep Turnover Falls to Pre-Pandemic Levels

Number of US Reps changing firms, 2015-2024

From channel to channel

The most common destination for departing reps was firms within the same distribution channel. However, a significant number of reps switched channels, drawn by higher payouts, improved access to technology, and closer alignment with client interests. Since the start of 2020, nearly 10% of wirehouse reps have moved to other channels, primarily to traditional and independent firms. While more reps joined than left independent firms overall, the channel was the largest source of new reps for retail investment advisors (Retail IAs), which as the table below illustrates, netted the largest gain from channel switchers.

Figure 2: Independent, RIA Segments Driving Growth

Licensed Rep Movement 2020-2024

A changing game

The movement of reps to independent and investment advisory firms stemmed from huge structural changes in intermediaries’ business models, which accelerated in the 2010s. The shift from commission- to assets under management (AUM) fee-based advice models accelerated as concerns over conflicts of interest from regulators and investors grew. The rise of robo-advisors accelerated the shift toward holistic financial advice, further challenging the viability of purely transaction-based models. The higher valuations associated with fee-based business models were also an attraction, especially for an aging advisor base looking to cash out. The proliferation of low-fee index ETFs—often the building blocks of model portfolios—further tarnished the appeal of higher-fee, commission-based investment offerings.

With the rules of the game shifting to AUM-fee based business models, the number of reps registered solely as broker-dealers sank. The chart below illustrates the impact: Over the past five years, broker-dealer registrations fell by approximately 50,000, an 18% decline. Traditional firms saw the largest falloff—a decline that reflects reps exiting the business, shifting channels, or becoming dually registered.

Figure 3: RIA Reps Surge, Broker-Dealer Only Plunges

Number of reps by registration type, 2019 and 2024

The number of dual registrants—that is, those registered both as a broker-dealer and a RIA—have crept upward in recent years by more than 11,000, or about 4%, since the start of the decade. Registering as both a broker-dealer and a RIA reflects advisors’ need to meet the higher standards of the 2019 Regulation Best Interest (Reg BI), while still serving transaction-based clients and to sell commission-based products like annuities. Together, these trends signal an industry increasingly defined by fee-based models, regulatory-driven accountability, and the need for advisors to balance transactional flexibility with fiduciary standards.

Looking ahead

The forces that have been driving reps to join other firms are unlikely to shift in the coming years. Certainly, structural factors like demographics, consolidation, and the bigger paydays associated with greater independence are not going anywhere. And while most advisors will likely not change firms, a small minority anticipate making changes to their practices that will fuel tomorrow’s rep movement.

For asset managers and other service providers, the landscape will continue to shift. Consolidation and increasingly centralized home offices have already narrowed the areas where intermediaries can be influenced. Meanwhile, the rise of independence and fiduciary standards has reshaped advisor practices, client interactions, and portfolio construction. Adapting will require not only new engagement strategies, but also the flexibility to reach advisors wherever they move next.

Readers can click here to read the full February 2025 Rep Movement Report, which is now available on the ISS MI Market Sage platform.

By: Christopher Davis, Vice President, ISS Market Intelligence