To borrow a phrase from the late Queen Elizabeth II, most asset managers will be unable to look back on the first half of this decade with undiluted pleasure.

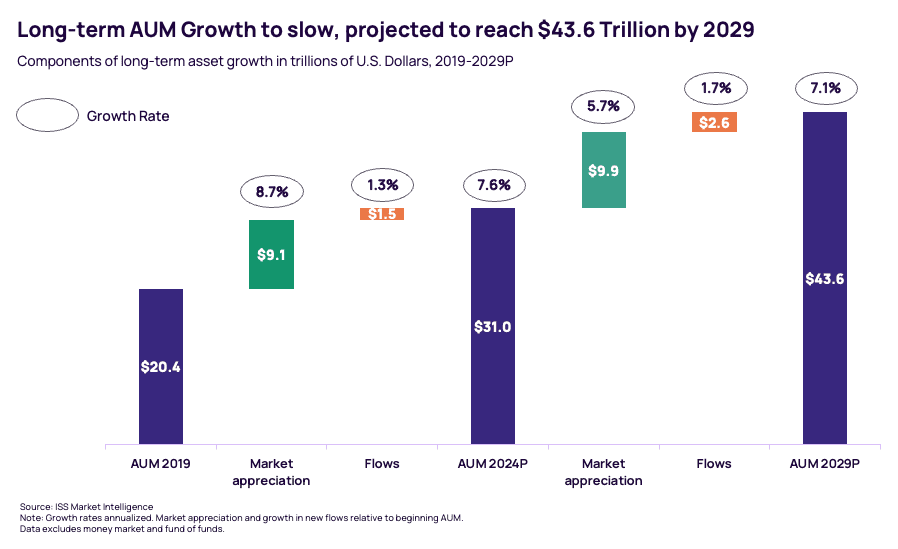

Indeed, asset managers will remember a global pandemic, two bear markets, political tension on all fronts, and a speculative frenzy that largely left them sitting on the sidelines. Sure, long-term assets under management (AUM) are expected to have grown at a respectable 8.7% annual clip by the end of 2024, but they will also remember the $1.5 trillion is projected to bleed out of active funds by the end of this year. The expected windfall from an aging population eluded active bond managers thanks to soaring yields and record outflows in 2022. Although market appreciation is projected to lead to boosted growth, these gains were heavily concentrated in U.S. stock funds, particularly the tech-heavy stocks.

Will managers look more fondly upon the next five years? The chart below, which summarizes ISS MI’s asset and flow forecast through 2029, depicts a mixed future. On one hand, the forecast, detailed in the 2024 State of the Market: Future of Retail Products report, anticipates weaker U.S. stock market performance to slow asset growth to a 7.1% annualized pace over five years. On the other, it foresees more opportunities for managers to grow sales. As lower yields reduce the appeal of holding cash, organic growth is expected to accelerate slightly, generating an additional $1.3 trillion in new sales over the next half-decade. Moreover, with most capital market forecasts anticipating a continued bond market recovery and a bounce back in non-U.S. stock markets, managers can expect stronger growth in places where it has been scarce.

Active managers may still face an uphill climb. Active mutual funds’ aging shareholder bases are expected to continue to shrink as new sales flow to ETFs—mainly index funds. While interest in active ETFs will likely not grow anywhere quickly enough to make up for these losses, active fund buyers’ shift from mutual funds to ETFs could well put a giant pot of assets—about $1 trillion in net active ETF flows over five years—in play.

Not only do we anticipate the ETF market continuing to act as a proving ground for innovation over the next half-decade, but it will also be the field on which the biggest games are most often played. Advisors certainly see it that way: When ISS MI asked advisors in July 2024 where they would prefer to invest client assets if their favorite manager offered options across vehicle types, 60% chose ETFs, up from 53% two years prior. Enthusiasm for mutual funds waned further; the vehicle was the top choice for just 15% of surveyed advisors this year, down from 20% the prior year.

As active fund buyers increasingly shift to ETFs, more managers are likely to bring their active strategies to the space. While many fear cannibalizing their existing investor base, this concern could eventually be outweighed by the risk of losing market share to competitors. Additionally, expect managers to try escaping the zero-sum dynamics of traditional active management by carving out new market niches. A recent proposal from State Street and private equity giant Apollo to combine public and private debt in ETF packaging hints at the kinds of innovations to come.

The proposal is one emerging path in the race to bring private market access to retail investors. Semi-liquid structures such as interval funds and business development corporations take it a step further. In contrast to open-end funds, these products offer quarterly withdrawals and limit redemptions to a relatively small slice of AUM. These features have made it possible to bring private markets, particularly private credit, to a broader audience. Interval funds, for example, attracted $8.2 billion in net new cash in 2023 and another $10 billion through September 2024 according to data from ISS MI’s Simfund.

The race to private markets will expose traditional asset managers to new competitive dynamics—not just from conventional rivals but also alternative specialists, which benefit from their expertise and the perception of exclusivity. There will be more than one way to adapt to these expected changes. Some, like State Street, will partner with blue chip Alts players. Others will leverage their own capabilities, whether built or acquired in-house. Traditional managers will benefit from already-established relationships with advisors and gatekeepers and their historical experience in bringing new products to retail markets.

Looking ahead

Tomorrow’s fund buyers will gravitate to product types that either make investing cheaper and more efficient (ETFs), more personalized (SMAs), or better diversified (private market vehicles). While there will be many winning strategy options, all of them will require managers to adapt their investment and distribution strengths to this reality. Some will move up the value chain and partner with advisory firms, while others may go a step further, transforming into full-blown distributors or wealth managers themselves. The future of the asset management industry will be shaped by those who figure out what investors really want—and how to deliver it to the right buyers.

By: Christopher Davis, Head of U.S. Fund Research, ISS Market Intelligence

Simfund Enterprise subscribers can access the 2024 State of the Market: Future of Retail Products report on the ISS MI MarketSage platform. For more information about this report, or any of ISS MI’s research offerings, please contact us.