Defined contribution net flows in 2023 return to pre-pandemic levels

ISS Market Intelligence has released the latest edition in the Windows into Defined Contribution series. Drawing on the ISS MI BrightScope DC Plan database, this research covers the 763,000 DC plans in the US. The Q4 2024 edition examines the recovery in assets experienced by defined contribution (DC) plans across 2023.

The DC market’s rebound follows an exceptionally sharp decline from 2022. Returns fell across asset classes as the Federal Reserve engaged in the fastest rate-raising campaign in decades. Within DC plans, market losses in 2022 contributed to a $1 trillion decline in assets, pulling assets below where they had ended in 2020. Fortunately, recovering markets, supported by strong labor market activity, pushed 2023 assets to just below the market’s peak in 2021.

Plans ride market recovery

Assets in DC retirement plans stood at $8.4 trillion at the end of 2023, according to Form 5500 data released by the U.S. Department of Labor (DOL) and captured within the ISS MI BrightScope Defined Contribution plan database. This was a $1.1 trillion boost over 2022’s $7.3 trillion—itself a severe drop from 2021’s $8.6 trillion. Assets under management in the long-term mutual fund and ETF market recorded a similar trajectory, shrinking from $27.5 trillion in 2021 to $22.4 trillion in 2022 before bouncing back to slightly short of their previous record at $26.2 trillion in 2023.

2022 witnessed double-digit losses across asset classes, with the S&P 500 declining 18.1% and the Bloomberg U.S. Aggregate Bond index falling by 13.0%. While rate cuts would not arrive until the fall of 2024, the cessation of rate hikes allowed markets to stabilize and recover. Equity markets grew by 26.3%, while bonds recorded a gain of 5.5% in 2023. Investors within long-term funds responded to this by depositing a net $38.7 billion during 2023 after an unusually harsh year of redemptions in 2022, withdrawing $394.5 billion.

Redemptions moderate from pandemic levels

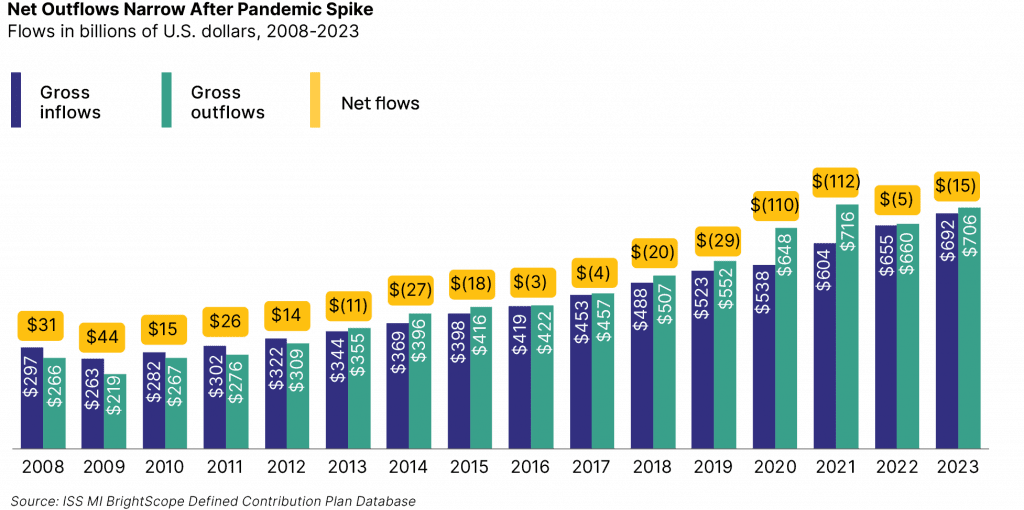

Retirement plans, however, did not record a similar recovery in sales over 2023. Net outflows, in fact, widened to $14.7 billion from $4.6 billion seen in 2022. Figure 1 (below) displays gross inflows, gross outflows, and net outflows since 2008. While net outflows did increase marginally, they were far below the spikes witnessed in recent years. 2020 and 2021 each saw net withdrawals surpass $100 billion as interruptions to labor markets slowed net contributions while pushing gross outflows past record levels. Despite significant headwinds in withdrawals, gross inflows have reached new records every year since 2009, supported from both the employer and participant side.

Figure 1: Net outflows narrow after pandemic spike

Flows in billions of U.S. dollars, 2008-2023

Source: ISS Market Intelligence BrightScope Defined Contribution Plan Database

Flows activity in retirement plans is more heavily influenced by shifts in demographics and labor markets than the year’s capital market returns. The consistent nature of most plan participants’ behavior leads to strong year-over-year contributions—a key appeal for asset managers who seek to include their funds among plan options. Given the strong roles played by auto-enrollment, auto-escalation, and the use of strategies with professionally-managed glide paths like target-date funds, market returns are less likely to be directly tied to DC participant decisions unless those returns are indicative of such a sustained macro downturn that individuals face increased job losses and separations from employer-provided plans.

The full report is available to subscribers on the MarketSage research portal. For more information about this report, or any of ISS MI’s research offerings, please contact us.

By: Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence